Research in Economics

Using the User Cost of Monetary Assets to Explain the Investment Portion of Gross Domestic Product

By Adam Bourgoin-Stone

Over the summer, I have been co-writing a paper with Dr. Biyan Tang on the merits of utilizing the user cost of monetary assets rather than the interest rate in economic research, specifically research into the investment part of Gross Domestic Product. The paper itself is not complete yet, and the current results may change if errors in the regression are detected. The paper has been submitted to present in a conference hosted by the Midwest Economics Association. This project has been and continues to be an incredible opportunity for me to not only learn more about economics, but also expand my critical reading and research skills.

Gross Domestic Product is often used in economics as an indicator of general economic growth. GDP is equal to Consumption + Investment + Government Spending + Net Exports. According to the Bureau of Economic Analysis, investment has remained at between 16% and 26% since 1947. Since investment is a significant portion of GDP, it is important to understand which factors correlate with it, and which factors can promote its growth. Based on traditional economic theory, the interest rate is negatively related to the level of investment that firms are willing to make. In other words, with a higher interest rate, investment will fall assuming other economic or political conditions remain the same. However, the relationship between the interest rate and investment can be unclear. Some research in the past has found a negative relationship; some has found a positive relationship; one paper found that the correlation changes significantly based on the interest rate level at the time of adjustment. A more intuitive tool for measuring investment as a part of GDP may be the user cost of monetary assets. The user cost is measured by the opportunity cost, or the forgone interest, of holding certain liquid monetary assets (like currency or checking account balance) versus holding pure investment assets. For example, if you held $1000 in cash, the user cost of your monetary asset would be the federal interest rate that you could have earned on the money had you kept it entirely in the form of investment assets such as treasury bonds. The user cost of monetary assets can be separated into the user costs for the various monetary aggregates, such as M1, M2, M3, and M4. A general overview of the monetary aggregates is that M1 contains the most liquid assets, and that each subsequent monetary aggregate contains the previous aggregate plus less liquid assets. For example, M1 contains physical currency, demand deposits, traveler’s checks, and other checkable deposits. M2 contains everything in M1, and also savings deposits, money market securities, mutual funds, and other time deposits.

Barnett (1978) derives a user cost formula for monetary assets:

where pit is the current period user cost of the per capita real balances of monetary asset i during period t, p*t is an aggregate index of the prices of good/services and of the prices of durable goods rental during period t, Rt is the yield on per capital bond holdings during period t, and rit is the nominal yield on monetary asset i during period t. The formula demonstrates that as the benchmark interest rate rises, the forgone interest rate increases with it.

The relationships of different economic factors with investment can be described using the Ordinary Least Squares regression

PriInv = b0 + b1(IntRate) + b2(rGDP) + b3(PubInv) +b4(PriCredit) + b5(CorpTax) + b6(Income) + b7(Inflat) + b8(TreasBond) + b9(Savings)

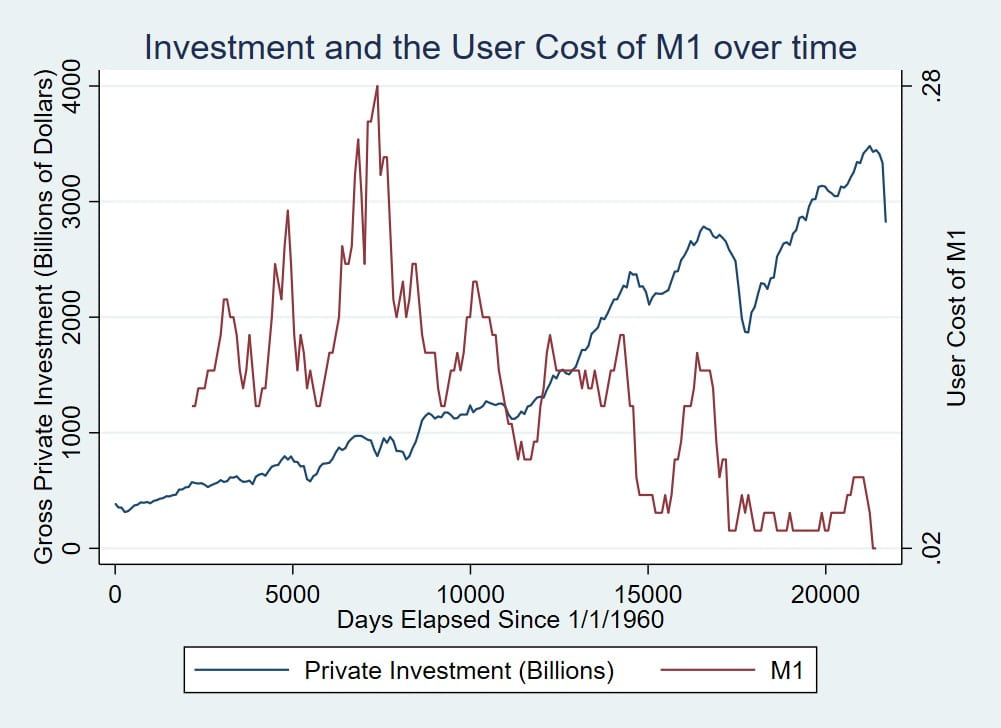

where the dependent variable is private investment in billions of dollars, and the independent variables are the interest rate, real GDP, public investment, credit available to the private sector, the effective corporate tax rate, aggregate income, the inflation rate, the treasury bond yield rate, and the savings rate. The user cost data was organized by the user costs for the different monetary aggregates (e.g. M1, M2, M3, M4). Two regressions were used, one using the interest rate, and the other replacing the interest rate with the user cost of monetary assets for M1. The adjusted R2, which is the percent of the variance of the dependent variable that is explained by the independent variables, was compared to determine whether the user cost is a better determinant of private investment than the interest rate. Regressions were run with the user cost for each monetary aggregate, with the regression that yielded the highest adjusted R2, the user cost for M1, being compared with the interest rate regression. The t-values of the interest rate and the user cost for each monetary aggregate were used to determine the statistical significance of each variable’s correlation with gross private investment. The statistical significance of each monetary aggregate’s user cost and the interest rate is visualized in Figure 1. Clearly, the interest rate is shown to have the most statistically significant correlation with the investment, and the user cost for M1 is shown to have the most significant relationship out of all of the user costs, though it is still statistically insignificant. Figures 2 and 3 show the interest rate and the user cost of M1 over time with gross private investment, respectively. The user cost and the interest rate are shown to be almost identical in proportion.

Figure 1, t-values of the interest rate and the monetary aggregate user costs

Figure 2, gross private investment and the interest rate over time

Figure 3, gross private investment and the user cost of M1 over time

The coefficients of each of the variables of the regression using the interest rate are shown in Figure 4. In this regression the interest rate is found to have a positive correlation with private investment. While at first glance, this seems contrary to traditional economic theory, this is likely because we did not add a lag to the regression. The relationship is shown to be positive because when investments fall, the federal reserve lowers the interest rate to stimulate investment, and when investment rises again, the federal reserve slowly returns interest rates to their previous values. The effective corporate tax rate was also shown to have a positive correlation, when a higher tax rate would be expected to lower the funds firms have at their disposal to invest, thereby reducing private investment. Figure 5 shows the regression using the M1 user cost (as that is the user cost that had the most significant correlation with investment, and the regression using the M1 user cost yielded the highest adjusted R2). The effective corporate tax rate is shown to have a positive relationship in this regression as well. In fact, most of the variables have similar values to the regression using the interest rate, except for the treasury bond yield rate and the inflation rate.

Figure 4, regression results for the interest rate. Standard errors are below coefficient values. *** – significant at 1% level. ** – 5% level. * – 10% level

Figure 5, regression results for the user cost. Standard errors are below coefficient values. *** – significant at 1% level. ** – 5% level. * – 10% level

The adjusted R2 of the regression using the interest rate was .9905, and the adjusted R2 of the regression with the user cost was .9881. This result is not unexpected, given the fact that the user cost was found to be statistically insignificant, while the interest rate was found to be significant at the 0.1% significance level, meaning that there is only a 0.1% risk of concluding that it is significant when it isn’t.

According to these results, the interest rate is probably a better variable than the user cost for explaining the variance of investment in the US. Secondary results include the statistical insignificance of the inflation rate when explaining investment, and also the inconsistency of the treasury bond yield rate’s significance. When using the interest rate, it was found to be mostly insignificant, but when using the user cost for M1, it was found to be significant at or above the 1% level. Based on these current results, I cannot conclude that the user cost of monetary assets is a more efficient factor than the interest rate for analysis of the investment part of GDP.

I want to thank the Dean of the UMass Dartmouth College of Arts and Sciences, Dr. Pauline Entin, for the generous stipend that I was granted for my summer project.

Works Cited in Paper

Acha, Anthony, and Kelechi Acha. “Interest Rates in Nigeria: an Analytical Perspective.” Research Journal of Finance and Accounting, vol. 2, no. 3, 14 Apr. 2016, pp. 71–81.

Agu, Osmond Chigozie. “DETERMINANTS OF PRIVATE INVESTMENT IN NIGERIA: AN ECONOMETRIC ANALYSIS.” International Journal of Economics, Commerce and Management, vol. 3, no. 4, Apr. 2015.

Ahmed, Afaq, and Muhammad Mubarik. “Impact of Interest Rate and Inflation on Stock Market Index: A Case of Pakistan .” Jan. 2012.

Ajide, Kazeem, and Olukemi Lawanson. “Modelling the Long Run Determinants of Domestic Private Investment in Nigeria.” Asian Social Science, vol. 8, no. 13, 2012.

Akhtar, M. A. “Effects of Interest Rates and Inflation on Aggregate Inventory Investment in the United States.” The American Economic Review, vol. 73, no. 3, June 1983, pp. 319–328.

Albu, Lucian Liviu. “TRENDS IN THE INTEREST RATE–INVESTMENT– GDP GROWTH RELATIONSHIP .” Romanian Journal of Economic Forecasting, vol. 3, Jan. 2006, pp. 5–13.

Appienti, William, et al. “KEY DETERMINANTS OF INVESTMENTIN GHANA: COINTEGRATION AND CAUSALITY ANALYSIS.” May 2016.

Awan, Rehmat, et al. “Rate of Interest, Financial Liberalization & Domestic Savings Behavior in Pakistan.” International Journal of Economics and Finance, vol. 2, no. 4, 2010.

Bagci, Erdem, and Emre Erguven. “Relations between Interest Rate, Inflation, Growth AndInvestment in Turkey, 2002-2015 .” 2016.

Bitros, Georgios, and M. Ishaq Nadiri. “Elasticities of Business Investment in the U.S. and Their Policy Implications : A Disaggregate Approach to Modeling and Estimation .” July 2017.

Chen, K. C., and Daniel Tzang. “Interest-Rate Sensitivity of Real Estate Investment Trusts.” The Journal of Real Estate Research, vol. 3, no. 3, 1988, pp. 13–22.

Heim, John. “THE INVESTMENT FUNCTION: DETERMINANTS OF DEMAND FOR INVESTMENT GOODS.” Jan. 2008.

Kosma, Olga. “Determinants of Investment Activity: the Case of Greece.” 2015.

Maccini, Louis, et al. “The Interest Rate, Learning, and Inventory Investments.” American Economic Review, vol. 94, no. 5, Dec. 2004, pp. 1303–1327.

Magableh, Sohail, and Sameh Ajlouni. “Determinants of Private Investment in Jordan: An ARDL Bounds Testing Approach.” Dirasat, vol. 43, no. 1, Jan. 2016.

Mueller, Glenn, and Keith Pauley. “The Effect of Interest-Rate Movements on Real Estate Investment Trusts.” Journal of Real Estate Research, vol. 10, no. 3, Feb. 1995, pp. 319–326.

Munir, Rahila, et al. “Investment, Savings, Interest Rate and Bank Credit to the Private Sector Nexus in Pakistan.” International Journal of Marketing Studies, vol. 2, no. 1, 2010.

Noman, Muhammad. “Rate of Interest and Its Impact on Investment to the Extent of Pakistan .” Sept. 2018.

Obamuyi, Tomola, and Sola Olorunfemi. “Financial Reforms, Interest Rate Behaviour and Economic Growth in Nigeria.” Journal of Applied Finance & Banking, vol. 1, no. 4, 2011, pp. 39–55.

Olweny, Tobias. “The Effect of Monetary Policy on Private Sector Investment in Kenya.” Apr. 2012.

Opreana, Alin. “THE LONG-TERM DETERMINANTS OF INVESTMENT: A DYNAMIC APPROACH FOR THE FUTURE ECONOMIC POLICIES.” Studies in Business and Economics, vol. 5, no. 3, Jan. 2010, pp. 227–237.

Oriavwote, Victor, and Dickson Oyovwi. “Interest Rate and Investment Decision in Nigeria: A Cointegration Approach.” American Journal of Business and Management, Mar. 2014.

Osei-Assibey, Eric, and William Baah-Boateng. “Interest Rate Deregulation and Private Investment: Revisiting the McKinnon-Shaw Hypothesis in Ghana.” The IUP Journal of Applied Economics, vol. 11, no. 2, Apr. 2012, pp. 12–30.

Pelgrin, Florian, and Sebastian Schich. “PANEL COINTEGRATION ANALYSIS OF THE FINANCE-INVESTMENT LINK IN OECD COUNTRIES.” Document De Travail De L’OFCE, Jan. 2002.

Peng, Liang, and Thomas Thibodeau. “Interest Rates and Investment: Evidence from Commercial Real Estate.” Journal of Real Estate Finance and Economics, vol. 60, no. 4, 1 May 2020.

Peter, Audu, and Oluwoyo Temidayo. “Testing the Validity of McKinnon-Shaw Hypothesis: Empirical Evidence from Nigeria.” Asian Journal of Economics, Business and Accounting, vol. 2, no. 2, 2017, pp. 1–24.

Sharpe, Steve, and Gustavo Suarez. “Why Isn’t Investment More Sensitive to Interest Rates: Evidence from Surveys.” 1 Oct. 2015.

Tan, Willie. “GNP, Interest Rate and Construction Investment (Tan 1987).” Construction Management and Economics, vol. 6, no. 3, 28 July 1988, pp. 185–193.

Udah, Enang. “MACROECONOMIC REFORMS, GOVERNMENT SIZE, AND INVESTMENT BEHAVIOR IN NIGERIA: AN EMPIRICAL INVESTIGATION.” European Journal of Social Sciences, vol. 33, no. 2, Aug. 2012.

Waheed, Abdul. “Determinants of Domestic Private Investment: Test of Alternative Hypotheses for Pakistan.” International Journal of Research in Business and Social Science, 2015.